Real Estate Paperwork Is Boring… Until It Decides Who Gets the House

- Tenley Cotten

- Jul 6

- 10 min read

Updated: 4 days ago

The note, the deed, the mortgage, the title company, and the documents quietly doing the heavy lifting.

Real estate paperwork has a reputation for being boring, and honestly, I get it.

Nobody sees a stack of closing documents and thinks, “Finally, my moment.” Most people think, “That’s a lot of pages; how long will this take?” or “Please tell me this pen is not about to run out.” Fair. But buried inside that stack are documents that actually matter. Like, really, really matter.

Some documents create promises. Some transfer ownership. Some tie a loan to the property. Some help protect the lender. Some help protect the buyer. Some are basically the paperwork equivalent of a tiny legal seatbelt.

So yes, real estate paperwork may look boring.

But it is only boring until it decides: Who owns the house, who gets paid, what secures the loan, and what happens if things go sideways. Let’s talk about the main players in a real estate closing: the people, the paperwork, and the plot twist documents quietly doing the heavy lifting.

1. The Buyer/Borrower: The One Making the Big Promise

The buyer, or borrower, is the person buying or refinancing the property and agreeing to repay the loan. In a financed real estate transaction, the borrower is not just “signing a bunch of papers.” They are making a legal promise to repay money, usually a lot of money, over a long period of time. Casual Tuesday. The borrower’s biggest promise usually appears in the promissory note.

Coolest thing about the borrower?

The borrower is the reason the whole transaction is moving. Without the borrower’s promise to repay, there is no loan to secure, no lender to protect, and no mountain of paperwork for everyone to lovingly wrestle into order.

2. The Promissory Note: The Promise to Pay

The promissory note is one of the most important documents in the loan package.

Plain-English version:

The note says, “I promise to repay this loan.” That is the borrower’s written promise to pay the lender back according to the loan terms.

The note usually includes important loan details like the loan amount, interest rate, payment terms, and what happens if the borrower does not pay as agreed.

Coolest thing about the note?

The note is the promise. Tiny document. Massive commitment. Like a pinky promise, but with underwriting.

3. The Lender: The One Bringing the Money

The lender is the bank, mortgage company, credit union, or other party providing the financing. The lender is basically saying, “I will lend you this money, but I need legal protection if you do not pay it back.” Because, respectfully, “trust me, bro” is not how mortgage lending works.

That is where the mortgage or deed of trust enters the chat.

This document gives the lender a security interest in the property, meaning the property is collateral for the loan. In other words, the promise to repay now has backup dancers — and one of them is the house. The CFPB explains that a security interest is what lets the lender foreclose if the borrower does not pay back the money borrowed. The CFPB also notes that the document giving the lender this security interest may be called a Mortgage, Deed of Trust, or Security Instrument.

Coolest thing about the lender?

The lender does not just hand over money and hope for the best.

The lender’s role is backed by documents that help protect its interest in the property if the borrower defaults.

Very serious. Very “I brought paperwork.”

4. The Mortgage or Deed of Trust: The Plot Twist Document

This is where things get juicy.

A mortgage and a deed of trust are both types of security instruments. Fannie Mae explains that security instruments for conventional mortgages include mortgages, deeds of trust, and security deeds, and that lenders must use the correct security instrument for the applicable jurisdiction, mortgage type, lien type, property type, and transaction type.

Plain-English version:

The note is the promise to repay. The mortgage or deed of trust ties that promise to the property. So when someone says the property “secures the loan,” this is what they mean:

The property is collateral. The borrower is saying:

“I promise to repay this loan, and this property backs up that promise.”

That does not mean the lender can skip the law, kick open the door, and yell, “Mine now!”

Absolutely not.

Please picture me standing there with a clipboard saying, “Sir, there is a process.”

It means that if the borrower defaults, the lender has a legal path to enforce its security interest through foreclosure. The CFPB explains that foreclosure processes differ by state and are generally done in two ways: judicial foreclosure, which involves filing a lawsuit, and nonjudicial foreclosure, which may happen without going to court in some states.

Coolest thing about the mortgage/deed of trust?

It gives the promise teeth.

Not vampire teeth.

Legal teeth.

Slightly less dramatic, but still important.

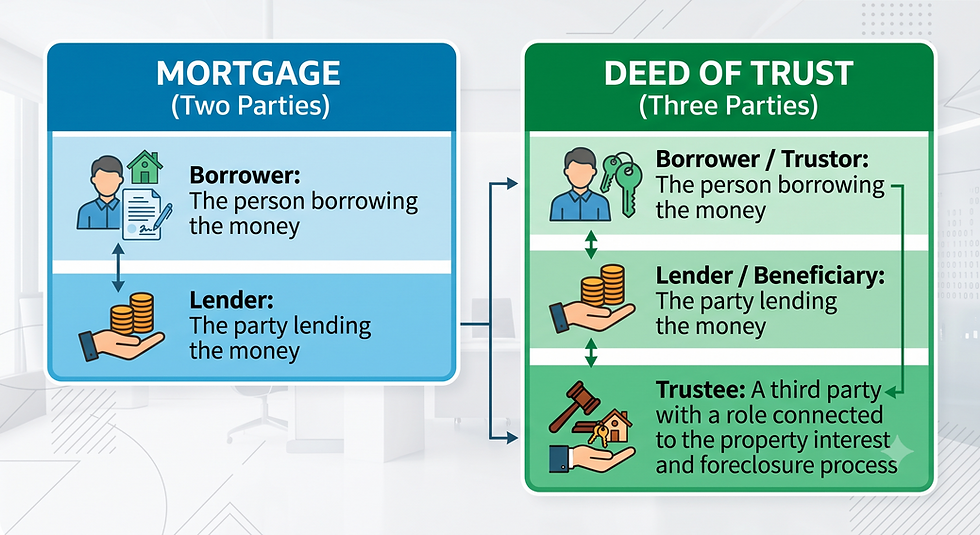

5. Mortgage vs. Deed of Trust: Same Job, Different Machinery

A mortgage and a deed of trust do a similar job: they secure a loan with real estate.

But they are not exactly the same.

Cornell’s Legal Information Institute explains that a deed of trust involves a borrower, lender, and trustee, and is used in some states instead of a mortgage. Cornell also notes that deeds of trust almost always include a power-of-sale clause, which allows the trustee to conduct a nonjudicial foreclosure without first getting a court order.

Tenley translation:

A mortgage is usually borrower + lender. A deed of trust says, “Cute. I brought a trustee.”

Why does that matter?

Because foreclosure may work differently.

With a mortgage, foreclosure often goes through the court system.

With a deed of trust, many states allow nonjudicial foreclosure, meaning foreclosure may happen outside of court if the document and state law allow it. Cornell explains that in nonjudicial foreclosure, the trustee or mortgagee may use a power of sale to foreclose without court action or authorization.

Again, that does not mean “no rules.”

It means a different legal process.

Still serious. Still regulated. Still not a free-for-all in a tiny foreclosure cowboy hat.

The Promise + Security Instrument

The note is the promise. The mortgage or deed of trust gives the promise teeth.

Accessible Long Description: A comparison infographic titled 'MORTGAGE (Two Parties)' and 'DEED OF TRUST (Three Parties)' with illustrations. On the left (MORTGAGE): two roles are shown—Borrower (borrowing money) and Lender (lending money)—with direct interaction. On the right (DEED OF TRUST): three roles—Borrower/Trustor, Lender/Beneficiary, and Trustee, who is involved with property interest and foreclosure. The Trustee holds keys and a gavel, indicating complex interactions among the parties.

6. The Deed: The Ownership Taxi

Now let’s talk about the deed, because this one gets confused with “title” all the time.

The deed is the document that transfers ownership interest in real estate from one party to another.

Plain-English version:

The deed moves ownership from the seller to the buyer. Title is the ownership/right.

The deed is the document that transfers it.

Coolest thing about the deed?

The deed is the ownership taxi. 🚕It is not the title itself. It is the document that says:

“Ownership is moving from this person to that person.”

Very official. Very important. Honestly, very dramatic for a piece of paper.

7. Title: The Ownership Situation

Title is not usually one single document sitting there like, “Hello, I am title.”

Title is the legal ownership/right to the property. When people talk about “clear title,” they usually mean the ownership history and property records do not show problems that would interfere with the transfer, like certain liens, claims, judgments, unpaid taxes, or ownership issues. This is why title companies do title searches.

They are checking the property’s history to make sure the person selling or refinancing has the right to do so, and that no land-records goblins are hiding in the bushes wearing a tiny hat.

Coolest thing about title?

Title is the ownership story. The deed may transfer ownership, but title is the bigger legal picture of who has rights in the property.

8. The Title Company: The Paperwork Detective

The title company is one of the major behind-the-scenes players in a closing.

Depending on the transaction, the title company may help coordinate the closing, perform or arrange the title search, prepare or collect documents, handle settlement funds, issue title insurance, and help make sure the closing process moves properly.

Plain-English version:

The title company helps make sure the property can transfer and the closing can happen. They are not just “the place sending paperwork.”

They are more like the paperwork detective, traffic controller, document wrangler, and “please nobody panic” department all rolled into one.

Coolest thing about the title company?

They look backward so the transaction can move forward.

That title search is not just busywork. It helps uncover whether anything in the property’s history needs attention before ownership changes hands or a lender’s interest is secured.

9. The Notary Signing Agent: The Calm Person With the Stamp

And then there is the notary signing agent.

Hi. Hello. This is where I enter with my stamp, my journal, my ID-checking eyeballs, and my emotionally supportive stack of sticky notes.

A notary signing agent helps guide the signing appointment. The signing agent may identify documents, point out where signatures, initials, and dates are needed, administer oaths when required, complete notarizations, and help ensure the package is signed and returned properly.

But the role is bigger than just “watch someone sign papers.”

In many real estate transactions, the notary signing agent is the only face-to-face person the signer ever meets. The lender may be on the phone. The title company may be in another office. The signing service may be coordinating behind the scenes. But when the signer finally sits down with that stack of documents, the person in front of them is often the notary.

That means the notary is representing a few very important entities at once: the hiring party, the title or escrow team, the lender, and the integrity of the signing process itself.

And just as importantly, the notary is also there for the signer.

Not as an attorney. Not as a loan officer. Not as someone giving legal or financial advice.

But as the calm, prepared professional who can read the room, slow the pace when needed, explain the flow of the appointment, and keep things from turning into a paperwork haunted house.

Because sometimes signers are nervous. Sometimes they are overwhelmed. Sometimes they are tired, confused, frustrated, emotional, or signing documents for one of the biggest transactions of their lives.

A good notary signing agent has to know how to stay steady.

We have to catch missing signatures, spot incomplete notarizations, follow instructions, protect private information, handle time-sensitive documents, avoid unauthorized legal advice, and still be warm enough that the signer does not feel like they are trapped in a financial escape room.

No pressure. Just a casual Tuesday with legally significant paperwork.

Coolest thing about the notary signing agent?

The notary signing agent helps protect the integrity of the signing while also helping the signer feel guided, respected, and not completely abandoned in a sea of documents.

A good notary is not “just the stamp.”

A good notary is the person keeping the appointment clear, calm, compliant, and moving forward — often while representing several behind-the-scenes parties the signer never meets.

10. Why Any of This Matters

It matters because these documents are not just “closing papers.”

They each have a job.

The note creates the promise to repay.

The mortgage or deed of trust secures that promise with the property.

The security interest gives the lender a legal claim tied to the property if the borrower defaults.

The deed transfers ownership.

The title company helps examine and coordinate the ownership transfer.

The notary/signing agent helps make sure the signing and notarizations are completed properly.

So yes, real estate paperwork can look boring.

But inside that boring stack are documents deciding ownership, debt, collateral, legal rights, lien priority, and what happens if things go sideways.

Very calm on the outside.

Very “main character energy” on the inside.

The Takeaway

The next time someone says, “It’s just paperwork,” remember:

Real estate paperwork is boring… until it decides who gets the house.

The note, the deed, the mortgage, the title company, and the security instrument are not just random pages in a closing package. They are the main characters in a transaction where ownership, money, and legal rights are all moving at the same time.

And if you are signing real estate documents, it is okay not to know every term before you sit down.

That is why good professionals matter.

A good lender can answer loan questions.

A good title company can answer title and settlement questions.

A qualified attorney can answer legal questions.

And a good notary signing agent can help guide the signing process clearly, calmly, and carefully — without making you feel like you accidentally wandered into a legal textbook wearing sweatpants.

A quick note for title and escrow teams

For title companies, escrow officers, signing services, and lenders, the signing appointment is not just a formality. It may be the only face-to-face interaction the signer has with anyone connected to the transaction.

That matters.

A prepared notary signing agent can help protect the integrity of the signing by verifying identity, following instructions, catching missing signatures or initials, completing notarizations properly, protecting private information, communicating clearly, and keeping the appointment calm.

I know the signer’s experience reflects on more than just me. It reflects on the title company, escrow team, lender, and signing service behind the transaction.

That is a responsibility I take seriously.

Tiny stamp. Big responsibility.

Need signing coverage in Central Pennsylvania?

The Roaming Pen LLC provides mobile notary and loan signing services in Central Pennsylvania, including Blair, Bedford, and Cambria Counties. I work with signers, title companies, escrow teams, lenders, and signing services to help closing appointments stay clear, calm, and complete.

Sources

Consumer Financial Protection Bureau, “What is a security interest?”

Consumer Financial Protection Bureau, “How does foreclosure work?”

Fannie Mae Selling Guide, “Security Instruments for Conventional Mortgages”

Cornell Legal Information Institute, “Deed of Trust”

Cornell Legal Information Institute, “Nonjudicial Foreclosure”

Cornell Legal Information Institute, “Mortgage”

Disclaimer

This post is for general educational purposes only and is not legal advice. Real estate laws, foreclosure procedures, document requirements, and title practices vary by state and transaction type. If you have questions about your legal rights, loan terms, foreclosure, title, or the legal effect of any document, contact a qualified attorney, lender, or title professional.

Comments